Harding Loevner

Global and emerging-markets quality-growth equity insights from Harding Loevner.

United States5 articlesLast published 10 Jun 2026

Equities

Research

Harding LoevnerEquities

Boomer Retirement Wave Gives Price-Conscious Acquirers an Edge - Harding Loevner

Harding Loevner examines how serial acquirers Diploma, Halma, HEICO, and Legrand are capitalising on a demographic-driven wave of small-business ownership transfers, securing below-market valuations from retiring founders who prioritise business continuity over price. The piece outlines the M&A playbook - including return discipline, direct negotiations, and programmatic deal frequency - that has allowed these industrial distributors to generate consistent shareholder value despite the general tendency of M&A to destroy it.

10 Jun 2026

Harding LoevnerEquities

How Apple Became an AI Winner - Harding Loevner

Harding Loevner analyst Kyle Levins argues that Apple, despite lagging peers in developing its own AI capabilities, is capturing more AI-related earnings than most companies through its App Store distribution monopoly and ~15% take rate on a surging volume of AI-driven app purchases and subscriptions. The piece examines the structural advantages of Apple's device ecosystem as AI commoditizes app development, and assesses risks such as agentic AI disintermediation and the potential emergence of AI-native hardware devices.

27 May 2026

Harding LoevnerEquities

Tracking AI’s Disruption of the Software Industry - Harding Loevner

Harding Loevner proposes three quantitative indicators - net retention ratio, sales efficiency, and CIO spending intent - to detect whether AI is materially disrupting the software industry's business model. Current readings across all three metrics show no definitive sign of broad disruption, though the piece flags the risk that these lagging signals may not provide investors sufficient warning time.

13 May 2026

Harding LoevnerEquities

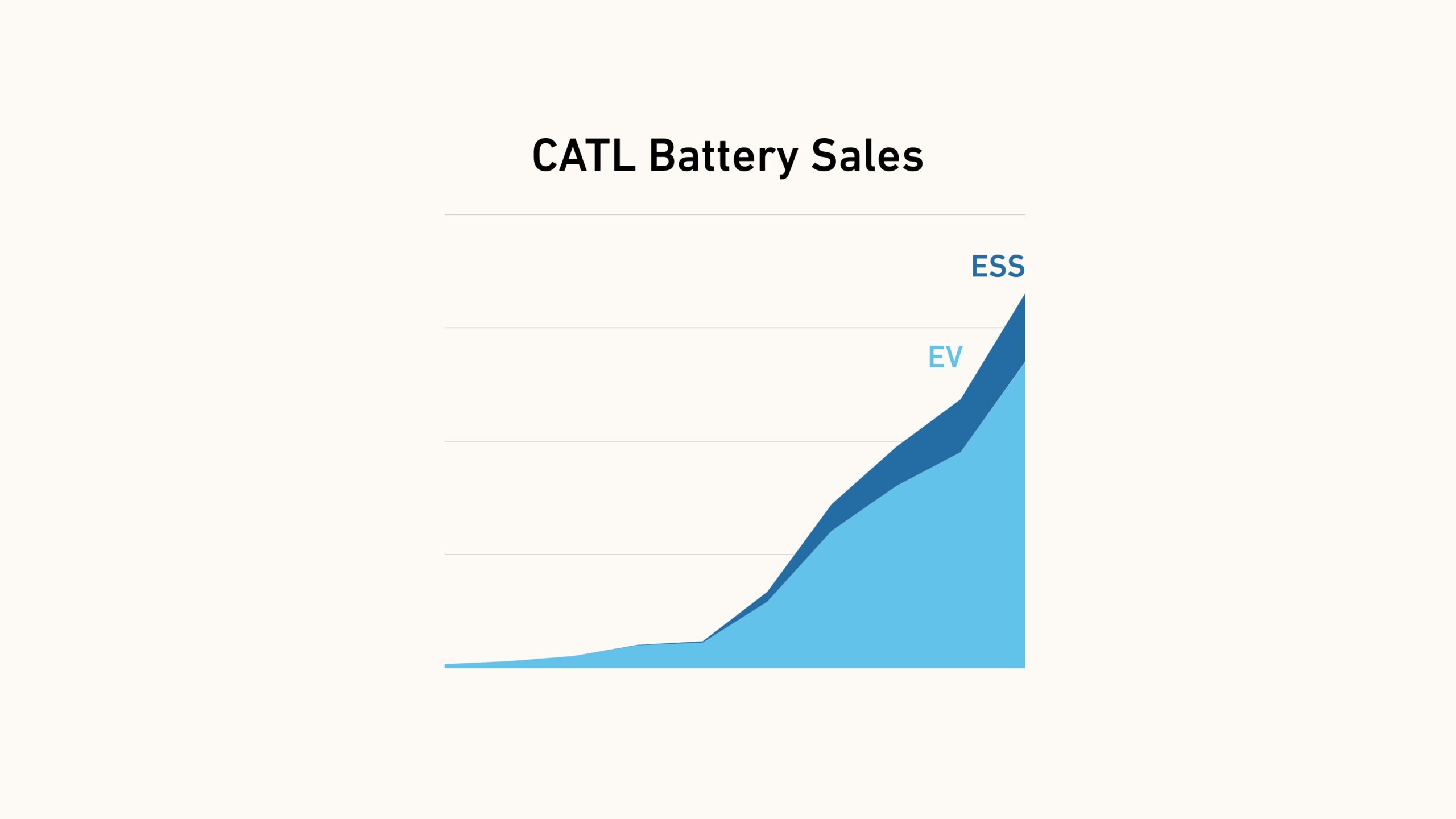

CATL’s Expanding Role in a Power-Hungry World - Harding Loevner

Harding Loevner examines CATL's competitive advantages in energy storage systems (ESS), including its ~40% market share in both EV batteries and the US ESS market, vertical integration, and R&D leadership. The piece argues that ESS - driven by renewable energy adoption and grid stabilization needs - is poised to become the dominant growth driver for CATL, potentially exceeding its EV battery business.

23 Apr 2026

Harding LoevnerEquities

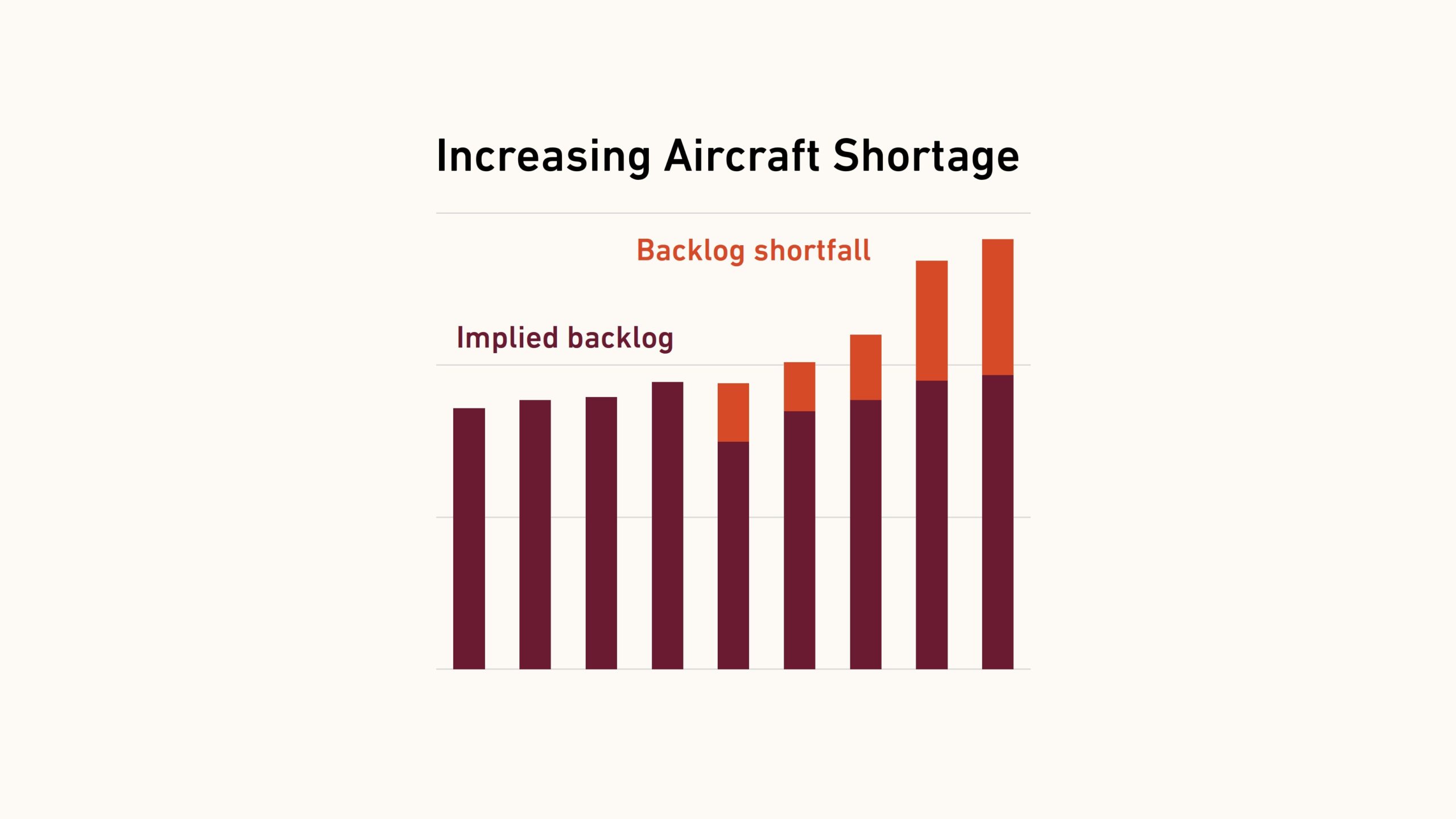

Aerospace Supply Crunch Favors Aftermarket Specialists - Harding Loevner

Harding Loevner argues that post-COVID aerospace production bottlenecks and an aging global fleet have created a structurally advantaged environment for aftermarket specialists such as Safran and HEICO. The piece details how engine manufacturers' monopoly-like economics on parts and servicing, combined with slow OEM-alternative adoption, support durable, high-margin earnings streams for aftermarket-focused companies.

21 Apr 2026